Cme futures date bitcoin

Contents:

CAC IBEX Stoxx Crude Oil Continuous Contract. Brent Crude Oil Continuous Contract. Natural Gas Continuous Contract. Heating Oil Continuous Contract. Gold Continuous Contract. Silver Continuous Contract. Copper Continuous Contract. Corn Continuous Contract. Wheat Continuous Contract. Soybeans Continuous Contract. Soybean Oil Continuous Contract. Soybean Meal Continuous Contract. Live Cattle Continuous Contract. Euro FX Continuous Contract. Japanese Yen Continuous Contract.

PRICING AND SETTLEMENT

British Pound Continuous Contract. Australian Dollar Continuous Contract. Canadian Dollar Continuous Contract. Eurodollar 3 Month Continuous Contract. Treasury Note Continuous Contract. Treasury Bond Continuous Contract. E-Mini Dow Continuous Contract. Tools Home. Stocks Stocks. Options Options.

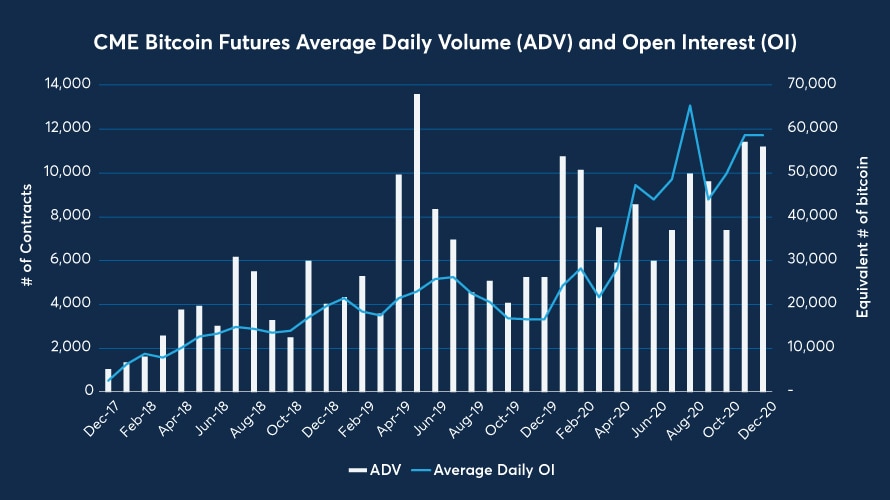

CME Group is the world's leading and most diverse derivatives marketplace. The company is comprised of four Designated Contract Markets (DCMs). Further. Learn about Bitcoin futures and options at CME Group, including contract specifications, benefits of trading Trade Date: 25 Mar | FINAL.

Futures Futures. Currencies Currencies. Trading Signals New Recommendations. News News. Dashboard Dashboard.

Tools Tools Tools. Featured Portfolios Van Meerten Portfolio. Market: Market:. Futures Menu.

Futures Expirations Calendar. Sat, Mar 27th, Help. Log In Sign Up. Stocks Market Pulse. ETFs Market Pulse. Therefore, Eq. Park and Hahn [] employ the superfluous regression approach to test the null hypothesis of the time-varying coefficient cointegration against the alternative of the spurious regression with non-stationary innovations. The corresponding test statistic is defined as:. In this paper, following the literature, we choose s to be 4.

In addition, we choose k from a range between 1 and 5. The optimal k is picked based on the adjusted R-square of CCR. The test statistic follows a Chi-square distribution with degree of freedom equal to the number of restrictions. It should be noted that the conditional variance-covariance matrix underlie the calculation of time-varying information share measures.

Most of the applications of BGARCH models for estimating the optimal hedge ratio assume that the error terms follow a bivariate conditional normal distribution. Typical distributional features of financial time-series data are excess kurtosis and asymmetry. In this paper, we employ a semi-nonparametric SNP approach to address the issue of excess kurtosis and non-zero skewness in the marginal return distribution.

In particular, a two-step estimation procedure is applied to obtaining estimates for the individual GARCH processes, conditional correlation matrix and marginal skewness and kurtosis parameters. First, the individual conditional variance equations are estimated via QMLE assuming Gaussian distribution and standardised innovations are obtained. Second, the parameters that capture the conditional correlation and other higher order moments are obtained via the log-likelihood maximization over the whole sample.

The log-likelihood of the multivariate SNP density that each observation at time t contributes to, without unnecessary constant components, is shown as:. R t is conditional correlation matrix defined by Eq. The procedure does not require pre-filtering the data but it require the maximum order of integration for the VAR. Using several unit root tests to check the stationarity of log futures and spot prices, we conclude that all variables are I 1.

The time-varying Wald test statistics for causal effects from Bitcoin spot prices to CBOE futures prices along with their bootstrapped critical values are shown in Fig. The two rows illustrate the sequences of test statistics obtained from the rolling window and recursive evolving procedures respectively, while the columns of the figure refer to the two different assumptions for the residual error term homoskedasticity and heteroskedasticity for the VAR. Sequences of the test statistics start from April Under different model and error assumptions presented in Fig.

As a result, date-stamping results from Figs. The result suggests that the CBOE spot market may not be able to lead the futures market since the former responds to new information more slowly than the latter. We can see that, first, there is little evidence of Granger causality episodes based on the rolling window procedure as presented in Fig. Second, the recursive evolving approach offers some different results.

CAC 40 0. Cryptocurrency News. The lead-lag relationship between cash and stock index futures in a new market. Effectively, we nest the static alternatives within our general, time-varying alternative, effectively rejecting the static null in favor of time-varying alternatives. Price discovery in interrelated markets.

As shown in Fig. As a result, the null hypothesis of no Granger causality can be rejected. Similarly, under the error assumption of heteroscedasticity, Fig. As noted in Shi et al. Next, therefore, we undertake our analysis using the CME futures prices and CME BRR to explore the causal relationship between futures and spot markets with the results presented as in Fig. For example, when we look at the date-stamping outcomes in Fig.

When the recursive evolving procedure is applied as in Fig. Finally, we conduct an analysis of Granger causality running from the CME futures to spot prices. Interestingly, we obtain significant evidence to reject the null of no Granger causality from the CME futures to spot prices as presented in Fig. The rolling window approach finds an episode of Granger causality between April and March in Fig. What is even more interesting is that the recursive evolving approach identifies an episode of Granger causality for the whole period between April and July as shown in Fig.

It is clear that our results are robust to different error assumptions. As the recursive evolving approach has higher power over the rolling window approach, we prefer the results obtained from the recursive evolving approach.

Bitcoin futures contracts at CME and Cboe | Reuters

Our results, therefore, suggest that the CME futures prices lead spot prices in the short term within the context of time-varying Granger causality. Our result suggests there exists bi-directional Granger causality between the CME Bitcoin spot and futures prices. More importantly, given the duration of the Granger-causal episodes and the magnitude of the test statistics in Fig.

From this we conclude that Granger causality runs from the futures market to the spot market. This result further suggests that the CME Bitcoin futures market leads the spot since the former embeds the new information faster than the latter. The results from time-varying Granger causality tests present some very important findings.

There are no Granger causality episodes running from the Gemini auction price spot prices to the CBOE futures prices;. The rolling window approach detects an episode April —March and recursive evolving approach detects an episode April —July running from the CME futures prices to spot prices;.

Bitcoin Futures and Crypto Market Data

There is bi-directional causal relationship between spot price and the CME futures prices;. Compared with duration of causal episodes and the magnitude of the test statistics in Fig. Overall, our result show that there is unidirectional Granger causality running from the CBOE Bitcoin futures to spot markets, whereas there is bidirectional Granger causality between the CME Bitcoin futures and spot prices.

It should be noted that even though Granger bidirectionality cannot be rejected, the Granger causality from the futures to spot is stronger than the other way around which suggests that the Bitcoin futures market dominates the spot in terms of strength of the lead-lag responses. Our results enrich the literature by identifying the evolving Granger causality relations between two major Bitcoin futures markets and their spot assets where both futures markets play a leading role in the dynamic Granger causality processes.

The result is in line with prior studies on traditional financial futures markets that indicate futures market lead the spot in the between-market interactive processes see, e. Next we use Park and Hann's [] procedure to test for the existence of cointegration which allows for the possibility of estimating a time-varying cointegrating coefficient. Via the Engle-Granger Theorem we know that cointegration implies Granger causality in at least one direction such that non-rejection of cointegration strengthens any causality results represented above, although the theorem does not itself identify the direction of Granger causality.

Upon the non-rejection of non-static cointegration, that is, a time varying equilibrium when cointegrated time series hold, a dynamic error correction process between them is identified. This further reinforces the accuracy and robustness of the results of price discovery given the more accurate estimation of error correction coefficients.

We also present the movements of the time-varying cointegration coefficients between the futures and spot markets in Fig. We, therefore, prefer the time-varying cointegration model rather than the time-invariant cointegration model. The Park Park and Hahn [] test results presented in Table 4 clearly show i that the null hypothesis that the cointegration specification, assuming a static cointegration relationship is statistically rejected, whereas ii the null hypothesis that the cointegration specification with a time-varying cointegration coefficient, governed by a FFF function of time, is not rejected at any conventional level.

The results hold for both futures markets. Our results therefore suggest that time variations in the cointegration coefficients exists, which has implications for the long-run equilibrium between spot and futures prices. Moreover, in Table 4 the null hypothesis that all the coefficients in the FFF time function are jointly zero is rejected, again for both of the futures markets, again supporting the results in terms of time variations of the cointegration coefficients.

Indices in This Article

Finally, we test three null hypotheses based on values of the variances of the cointegration coefficients. For the CBOE Bitcoin spot and futures markets, we test the null hypotheses that the variance equals 3. Note that the sample variance equals 3. The test result shows that the first null is rejected, whereas the null hypothesis that variance equals 3. These results suggest that the variance of the cointegration coefficient for the CBOE Bitcoin spot and futures is not zero, supporting time variability of that coefficient.

- Graphical abstract?

- 50000 eur bitcoin.

- chapman bitcoin;

- current price bitcoin usd?

- Bitcoin Futures & Crypto Spot Prices Real Time Market Data Feed?